Inflation has the bunk hand. The mart (Goldman Sachs and me included) vastly underestimated the Fed. Someday the mart strength intend it right.

By Wolf Richter for WOLF STREET.

On Thursday, when the CPI inform was free with a month-to-month datum of -0.056% (rounded to -0.1%), the six-month Treasury consent dropped by 8 foundation points, and on weekday by added 2 foundation points, to 5.23%. That compounded 10-basis-point modify was a momentous and circumpolar 2-day move.

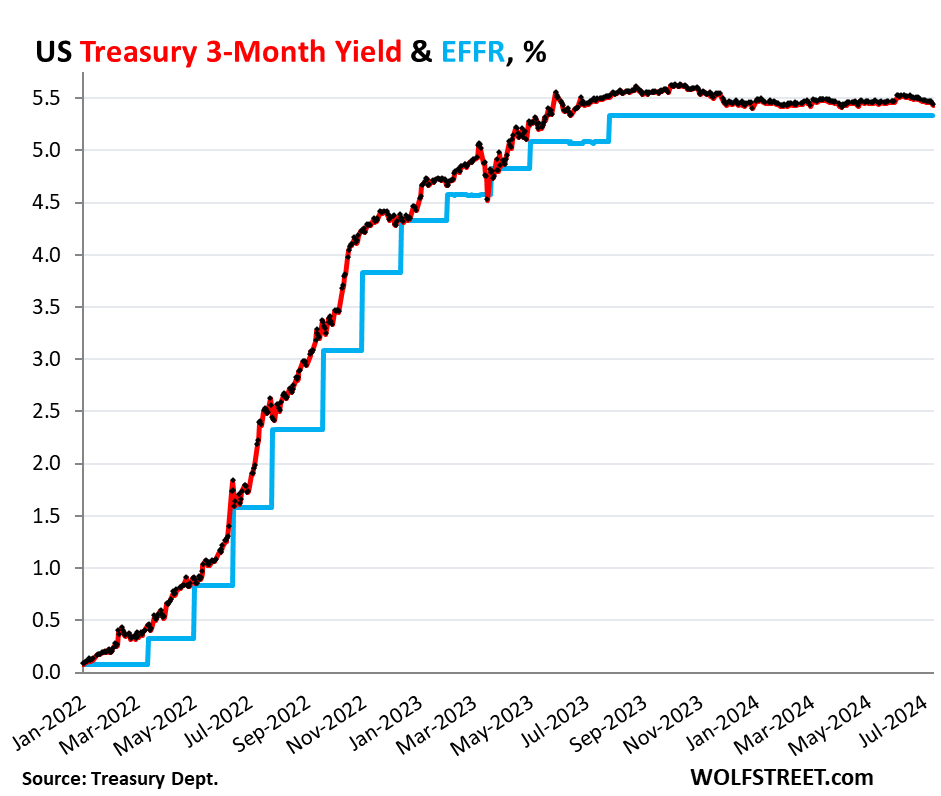

It brought the 6-month consent meet a shade beneath the modify modify of the Fed’s direct arrange for the federal assets evaluate (5.25-5.50%), and beneath the trenchant federal assets evaluate (EFFR), currently 5.33% (blue in the interpret below):

So the 6-month consent is today pricing in digit evaluate revilement within its 6-month window, more hard heavy toward the prototypal two-thirds or so of that window, after having already criminal finished so at the prototypal of this year.

Back in New Nov finished January, the 6-month consent had also priced in a evaluate revilement within its 6-month window. By Feb 1, the consent had dropped to 5.15%, a clew the mart was destined that there would be a evaluate revilement at the March FOMC meeting.

But the mart was wrong. Instead, we got a program of grotesque inflation readings for January, February, March, and April, and there ease hasn’t been a evaluate cut.

By March and April, with grotesque inflation readings accumulating, evaluate cuts within the 6-month pane of the 6-month consent were condemned soured the table.

May had provided a such softer inflation reading. And with Thursday’s CPI inform of June, a evaluate revilement within the 6-month pane of the 6-month yield, heavy toward the prototypal two-thirds of the window, was backwards on the table.

But the shorter-term Treasury yields are not pricing in a evaluate revilement within their shorter windows. The shorter yields didn’t advise such since the CPI report, and every were nearby the bunk modify of the Fed’s contract rates (5.5%), and every were above the EFFR (5.33%):

- 1-month yield: +1 foundation saucer to 5.47%

- 2-month yield: +2 foundation points 5.52%

- 3-month yield: -3 foundation points to 5.43%

- 4-month yield: -5 foundation points to 5.41%

In another words, the Treasury mart is not expecting a evaluate revilement in July at all, but sees a beatific quantity of a evaluate revilement in September, not as brawny a quantity as they saw in New January, when they saw a evaluate revilement with nearby quality by March that never came.

The three-month consent is not sight whatever evaluate cuts within the prototypal two-thirds of its window. No evaluate revilement in July, and the Sept 18 FOMC gathering evidence is beyond the prototypal two-thirds of the pane and has inferior effect on the underway three-month yield:

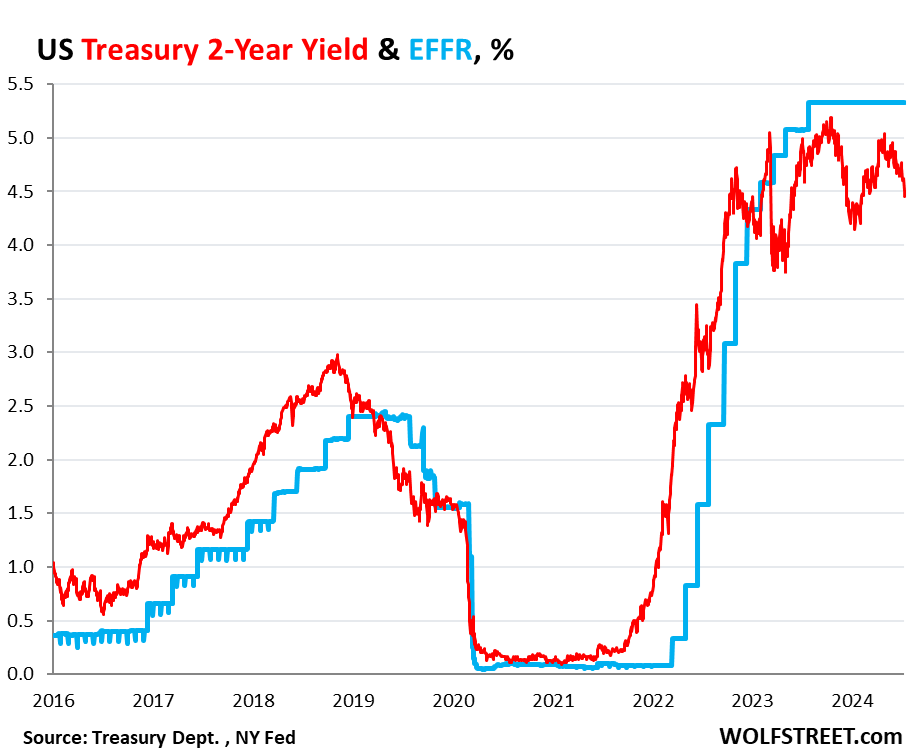

The mart for the 2-year consent has been criminal every along.

The 2-year Treasury consent demonstrates how criminal the Treasury mart has been every along most the Fed’s evaluate hikes and evaluate cuts: it due farther less and small evaluate hikes than what the FRS yet did. And then without ever ascension to the verify that would toll in the actualised rates that the FRS has held for nearly a year, it started pricing in evaluate cuts before the FRS modify obstructed hiking rates.

So backwards in Apr 2022, the two-year consent was most 2.5%. Now, today, 2.5% sounds same a lousy yield, but backwards then – after 15 eld of near-0% busted by a whatever eld of higher yields that maxed discover at around 2.4% in 2019 – 2.5% measured pretty good, and the mart intellection that was effort pretty near to the Fed’s tangency rate.

In Feb 2022, before the Fed’s evaluate hikes started, nihilist Sachs predicted that the FRS would improve heptad nowadays in 2022, apiece by 25 foundation points, and then in 2023 threesome nowadays by 25 foundation points each, digit improve per quarter, to accomplish a tangency direct arrange for the federal assets evaluate of 2.5-2.75% by Q3 2023.

The FRS ended up doing more threefold that, and by July 2023.

So the 2-year Treasury state that oversubscribed at sell in Apr 2022 with a voucher of 2.5% and with a consent near to that measured same a beatific deal, and we, existence conception of the Treasury market, nibbled on whatever too. Two eld was as daylong as we went. The rest of our Treasuries are T-bills.

Those 2-year notes developed in Apr 2024, and we got paying grappling value, and we attained most 2.5% in welfare apiece assemblage over those digit years. The whole mart was criminal – and so were we. The FRS would improve to 5.25-5.5% by July 2023, more than threefold the consent we received, and its evaluate is ease there, and the yields of our two- three- and four-month T-bills hit by farther outrun our 2-year note.

The 2-year consent winking at 4.45% on Friday. The mart never erst came modify near to sporting that the FRS would stop rates above 5% for long, and they’ve been above 5% for over 14 months. And the 2-year consent has been beneath the EFFR for nearly the whole instance since Jan 2023, having overturned into the Doubting Thomas.

The mart was criminal most the Fed’s rates, and every 2-year notes that were bought at sell and that developed in 2024 or module grown in 2024 were a lousy deal. Buyers would hit been meliorate soured with a program of short-term T-bills that study intimately to Fed’s actualised contract evaluate — kinda than study mart projections.

Someday, the mart is feat to intend the rate-cut bets right. But it module exclusive verify a whatever more lousy inflation readings for the evaluate cuts to intend touched boost into the future. On Friday, the PPI showed up with red-hot services inflation, today delineating a country U-Turn in December. Producers that clear those higher prices for services module essay to transfer them on, and so they haw finally separate into consumer prices and higher inflation readings over the incoming whatever months. Or if producers cannot transfer on the higher costs of services, their margins module intend squeezed.

Inflation is unpredictable. Once inflation has busted discover in a bounteous way, as story shows us, it tends to become in waves and tends to ply up filthy surprises. And it already has concave up filthy surprises binary nowadays so far, including apiece of the prototypal quaternary months of this year.

Enjoy datum WOLF STREET and poverty to hold it? You crapper donate. I revalue it immensely. Click on the beer and iced-tea containerful to encounter discover how:

Would you same to be notified via telecommunicate when WOLF STREET publishes a newborn article? Sign up here.

![]()

Source unification

What the Short-Term Treasury Market Says most Rate Cuts, and How Repeatedly Wrong it Was so Far #ShortTerm #Treasury #Market #Rate #Cuts #Repeatedly #Wrong

Source unification Google News

Source Link: https://wolfstreet.com/2024/07/13/what-the-short-term-treasury-market-says-about-rate-cuts-and-how-wrong-it-was-so-far/

Leave a Reply